Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Capitol Hill Hearings CSPAN December 6, 2012 8:00pm-1:00am EST

8:00 pm

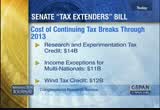

businesses get two types of income. active income, and passive income. active income is if the have a factory in china and sell cars. they can delay paying u.s. taxes on that indefinitely. but the money comes from the rent, as so-called passive income, they have to pay taxes on that immediately. this provision says if your a bank -- you can be late paying your taxes. it is going to be considered active income. it is quite valuable to them. it is kind of a gray area. in 1986 when they did big tax reform, they said that is active income and we should tax that money.

8:01 pm

host: we have been talking with sam goldfarb from cq roll call. thank you very much. >> explores the history and literary culture of all money -- of albany. tonight on c-span, a senate debate on the fiscal cliff. shaun donovan discusses it. harry reid and mitch mcconnell when back-and-forth on fiscal cliff issues and a proposal to raise the debt ceiling. here is part of their exchange. >> yesterday afternoon, i came to the floor and offered

8:02 pm

president obama's proposal on the fiscal cliff to show that neither he nor democrats in congress are acting in good faith in these negotiations. with just a few weeks ago before a potentially entirely avoidable blow to the economy, the president proposed a plan the members of his own party will even vote for. he is not interested in a balanced agreement, not particularly interested in avoiding the fiscal cliff, and clearly not interested at all in cutting any spending. with the president is really in, as we learned just yesterday, is getting as much taxpayer money as he can, first by raising taxes on small businesses who he believes are making too much money, and then on everybody else. not so he can lower the debt or the deficit, but so he can spend to his heart's content.

8:03 pm

for months, the president has been saying that all he wanted to raise taxes on the top 2% so he can tackle the debt and the deficit. however, yesterday, he finally revealed that that is not really is true intent. by demanding the power to raise the debt limit whenever he wants, by as much as he wants, he showed what he is really after is assuming unprecedented power to spend taxpayer dollars without any limit at all. this is not about getting a handle on deficits or debt or him. it is about spending even more than he already has. why else would you demand the power to raise the debt limit on his own? by the way, why on earth would we consider giving a president who has brought us four years of trillion dollar unchecked deficits of 30 to borrow? he is the last person who should have borrowing power.

8:04 pm

the only way we will cut spending around here is by using the debate over the debt limit to do it. now the president wants to remove that to cut all together. of course, it gets away -- it's in the wake of his spending plans. i assure you that will not happen. the american people want washington to get spending under control and the debt limit is the best tool we have to make the president take that demand seriously. the american people want us to cut spending. it is a fight they deserve and a fight we are willing to have bee. i am prepared to ask consent to allow the senate to vote on the president's bill limit proposal. i would ask this either as an amendment to the russian pr member that we will vote on this afternoon or as a freestanding bill if that is preferred.

8:05 pm

therefore, i now ask consent that it be in order to vote on an amendment which is the president's debt extension limit proposal. >> is there an objection? >> i have been thinking of how best to describe what has been having here in capitol hill for the last couple of weeks. every day, i get up and the first thing i read is the sports page. the sports page in "the washington post" is not as good as it used to be. there's always some good news and it is always on the sports page. due to the front page and get some of the bad news. but i -- but now i go to the

8:06 pm

front page and get some of the bad news. a team that is really fun to watch is the new york jets. coach ryan has a problem. he has three quarterbacks, sanchez, tim tebow, and a guy by the name of mcelroy. he cannot decide who their quarterback is going to be. that is the same problem the republicans are having. romney is gone, but he still in the background. we have mcconnell and we have the honor. who is the quarterback, mr. president? -- we have mcconnell and we have boehner. who is the quarterback, mr. president? we just had an election. the people overwhelmingly know why we have this debt. the polling right before the election showed that the vast majority of the american people

8:07 pm

realize that the debt was caused by george bush. that is a fact. mr. president, we have another judge report coming out tomorrow here we have a little problem because of what happened with hurricane sandy. but we will still have about 100,000 new jobs. we are approaching about 4 million jobs now that have been created. that does not merely make up for what was lost during the bush years, but we are making progress. people in america realize we cannot have a top-down economy that the republicans so glove during the bush years and they wanted to create begin with governor romney. mr. president, i would be happy to take -- and they want to have again beginning with governor romney.

8:08 pm

mr. president, i would be happy to take a look at the proposal. if that is what they want to do, i would be happy to seriously take a look at that and report to the white house and my caucus. but until then, i object. -- r. president >> that has been heard. >> the majority leader says that the republicans do not know who the quarterback is which is common when you do not have the president. but on the democratic side, you know who the quarterback is and he is throwing interceptions. we're moving backward and backward and backward toward the goal line from $4 trillion annual deficits and my friend from nevada still wants to blame that on george bush? and now he is asking for an unlimited authority to borrow

8:09 pm

whenever he wants to or whatever amount he wants to? >> majority leader. >> as a said, we would be happy to look at the proposal by my friend. but the president does not want to do anything other than what we have done before. and that is where we are now and that is why i would be happy to take a look at his proposal. that is what we did last summer. i would be happy to take a look at that and move forward on

8:10 pm

this. we democrats have a long line of republicans, as i outlined earlier on, where people make sure that the middle class and the port are taking care of. we have the calmness from "the move on.times," let's >> hours later, senator reid returned to the floor. >> i now ask unanimous consent that at 1:30 p.m. today, the senate did proceed to read s664, regarding the debt limit increase, that there be no limits [indiscernible] upon user yielding back at that time, the bill will --

8:11 pm

>> is there an objection? >> i reserve the right to object. what we're talking about is a perpetual debt ceiling grant in effect to the president. matters like this always require 60 votes. i would ask my friend, the majority leader, if he would modify his consent agreement to set the threshold at 60. >> majority leader? >> reserving a right to object. what we have here is republicans in the senate not taking is for an answer. this morning, the leader asked for consent on the proposal. now i am telling everyone to have that good, upper down vote. now he rejects his own idea. i guess we have a filibuster on the bill. so i object. >> is there an objection to the original request? >> yes, i reject.

8:12 pm

-- i object. >> whiplash. >> madame president. >> what just transpired deserves a word. senator mcconnell came to the floor this morning and offered a change in law that would help us avoid the kind of obstruction and the kind of showdowns we have had in the past over the debt ceiling. in fact, the idea was not new. it was his original idea that has been the law of the land that followed. and he offered and challenged senator reid to bring this matter for consideration by the senate. he said he would bring this to a vote in 20 minutes. and we would decide up or down whether the debt ceiling problem would be resolved once and for all under senator mcconnell proposal.

8:13 pm

and then senator mcconnell objected, say, no, no, we need 60 votes. for those who do not follow the senate, 60 votes is equivalent to a filibuster vote. so this may be a moment in senate history when a senator made a proposal, and when given a opportunity for a vote, he filibustered his own proposal. i think we have reached a new spot in the history of the senate we have never seen before. i will ask a parliamentarian to really look into this. i don't think this has ever happened before. but this calls into question if this was a kind of offer that would consider to be good faith. if senator reid offered to vote on it and senator mcconnell said no, that has to be a filibuster- proof revote >> i would ask my colleague to yield for a question. is it also correct that, basically, if we had voted, we would guarantee that we would not place the country again in a

8:14 pm

situation of defaulting on our bills and send a message that we can work together? the fact that we were willing to accept the republican leader's proposal and be willing to send a message that, as a senate, we want to make sure we have fiscal stability, that we're paying our bills, that this could be one step forward in making sure we can resolve the fiscal issues for the country. view of this as well? in fact, it would be an important message about stability? i have to say i share your amazement that the leader would, in fact, object to his own proposal and now be filibustering his own proposal that we were willing to accept as a bipartisan good faith effort for the country.

8:15 pm

did he not really just take us in the wrong direction? >> the republican senate leader, senator mcconnell, has such a strong appetite for the filibuster that we have seen 386 or 387 filibusters in the past six years. now he has decided that another good idea is to propose a bill and filibuster your own bill. i do believe that is history in the making. but that is why the epidemic for the filibuster in the senate has to change. what an abuse. we cannot have a vote on something that the republicans' proposed and the democrats were willing to vote for. this should make the news across america. it really is unfortunate. >> andy taylor covers congress for the associated press. what was he trying to do? >> i think he was trying to embarrass the democrats.

8:16 pm

he said the president's plan on the debt ceiling would allow the president to request whenever increases without the approval of congress. i guess he wanted to embarrass the democrats if they wanted to vote for it in election years. >> had the democrats respond? >> there is a lot of politics going on here. we just talked about the politics for the mcconnell side. i think the democrats are aware that, even if they get the republicans to crumble on raising tax breaks for a cure -- for upper bracket people, there will be a need to increase the

8:17 pm

debt limit in march. that is what speaker boehner uses as his leverage to a year and a half ago in his talks with president obama. i think there's a belief on the party democrats that they like to get this idea into come circulation. and they also want to manufacture some dialogue that the debt ceiling is not really the kind of leverage it was a year and a half ago. and you saw some of that from the president yesterday when -- or last week when he was talking about that he is not going to play that game may more. there is some of that. it turns out that the democrats would have enough votes to pass it through the senate. instead, senator mcconnell insisted that it requires 60 to get past the filibuster. >> on the republican side, how would a vote on either the

8:18 pm

fiscal cliff or raising the debt ceiling help the gop make their case? i am not entirely sure that it would. i am not sure hal and effective issue it would be pure >> the houses out now -- it would be. >> the house is out now. >> there is no public indication. you talk with some senators who yesterday were saying that not a lot is going on, more privately them publicly. but since then, we know that president obama and steve [indiscernible] spoke yesterday evening. the fact that neither side is leaking what happened on that call, you might say that they are trying to get back on track. they know that if they leak each

8:19 pm

other's confrontations, that is not good. there are only two participating really in this negotiation. and if they choose not to leak out that information widely, it is a speculation. >> what is the handle and how quickly could be brought -- what is the end goal and how quickly could be brought up for a vote? >> the goal is a down payment or some kind of thing for revenues, which is enough to get us past the fiscal cliff, turn off these automatic spending cuts and make sure that taxes don't go up. and then they would figure out what to do with the upper bracket. and then there would be a

8:20 pm

mechanism that would guarantee further action next year. if at all possible, they would disagree next year and there would be some sort of trigger or punishment for their lack of action. that sounds relatively simple, i think, putting it all together could take at least a couple of weeks after they have a deal. there could be some inevitable blocks either by conservatives in the house or in the senate. blowups either byow wha conservatives in the house or in the senate. the details can get pretty political party quickly. there's so much in flux.

8:21 pm

it all presupposes that the get an agreement. there was a school of thought that they could not get an agreement until tax rates actually go up next year. >> you can follow himat @apandrewtaylor. >> a discussion on the u.s. economy and you pull in the middle class with participants from think tanks, academia and business at 8:30 a.m. eastern tomorrow on c-span 2. >> the supreme court will look at what was passed in 2008 by a majority of six-three, i believe, and they will say that is president. and coming indiana had voter -- and indiana had voter i.d.. >> it was constitutional for

8:22 pm

them to establish id in the indian case. they did not say that all of those states -- >> let me finish. you misrepresented what i said. >> no, you let me finish. >> it is the law of this land your >> when i hear these accusations that black people, though her i'd be lost disproportionately affect minorities -- that voter i.d. disproportionate effect minorities, what are you telling black people? the somehow they are not good enough? their lesser then? that is what bothers me about a lot of the rhetoric coming from democrats and the left. that we always have to make special -- you know, there has to be a specialist when we deal with minorities because they are

8:23 pm

too feeble minded. we really need to make concessions for them because they cannot follow the rules like everybody else. and when you treat people like victims, i don't think they want to inspire pierre >> the editor and -- to is -- to aspire. >> the editor and founder of blackchick.com. >> senator bob casey cheers this joint economic committee hearing. it is one hour and 45 minutes.

8:24 pm

>> the committee will come to order. we want to thank everyone for being here today. i did not have a chance to personally greet our witnesses, but i will have time to do that later. i want to thank both of our witnesses for being here. i will have an opening statement that i will make, and then i will turn it to dr. burgess. i know that vice chairman brady will be her as well. we know the challenges that we confront here in congress on a whole range of issues, which are sometimes broadly described under the umbrella of the terminology, fiscal cliff. when we confront those difficult challenges, we have to ask ourselves a couple of basic questions. one of the basic questions we must ask is, what will be the result and will be the impact as it relates to middle income families? what will happen to them in the midst of all these tough issues we have to work out?

8:25 pm

we know there is broad agreement that going over the so-called fiscal cliff would jeopardize the economic recovery. it would do that by increasing taxes on families, halting employment growth, driving unemployment up instead of down, triggering a deep cuts to programs that families across the country count on. the job before the united states congress is to reach an agreement that builds on the economic progress that we are making, and puts us on a path to fiscal stability. we need to cut more spending, and generate more revenue. we need to do it in a smart way that keeps our economy growing. earlier this year, congress extended the payroll tax cut through 2012. the two percentage point payroll tax cut has played an important role to sustain the recovery. boosting economic growth by an estimated 0.5% of one percentage point, and creating 400,000 jobs.

8:26 pm

we should continue the payroll tax cut through 2013, and yesterday i introduce legislation that would keep the employee payroll tax at 4.2% next year. to keep the economy growing -- there is good evidence of that in the last couple of months? job growth of about 511,000. to keep that momentum going, we should provide tax credits to small businesses. that add jobs or increase wages from year to the next. my legislation includes such an incentive for small businesses to grow. i am confident that congress will again be successful in reaching a compromise in the days ahead. i look forward to hearing today from the experts that we have before us today on how to

8:27 pm

reduce the deficit while protecting middle income families. as we enter the holiday season, americans should not have to face the uncertainty that many will face with regard to their taxes. there is no reason that middle income families should go into this holiday season without knowing whether their taxes will go up next year. last year, democrats and republicans work together to cut nearly $1 trillion of spending. now we need to continue that bi-partisan work to cut more spending, and to bring in additional revenues. if congress fails to reach an agreement under the budget control act of 2011, $1.2 trillion in automatic spending cuts will take place between 2013 and 2021. republicans and democrats agree that indiscriminate across-the- board cuts is not the right and to do at this time in our nation's history.

8:28 pm

if we trigger the automatic spending cuts and tax increases, gross margin bottom will fall by half a percentage point. we will reverse the hard-fought gains over the past few years. we cannot afford to go backwards. instead we need a balanced and bipartisan approach. one that balances the short and long-term needs, distinguishes between foreign investments and the core investments that must be reserved, and spending that we can live without that utilizes both spending cuts and revenue increase. the first order of business should be to protect those middle income families i talked about and protecting them from a tax increase. the cbo estimates that simply extending the middle-class tax cuts would boost gdp by 1.3% and create 1.6 million jobs.

8:29 pm

let me say that again -- boosted gdp by 1.3% and create 1.6 million jobs from that tax cut we can enact. it would resolve much of economic safety for these middle-class families. the wealthiest among us can help us reduce the debt by paying more. it is encouraging to see republican members of the house and the senate speak out on the need or a deficit approach that includes raising taxes on wealthy individuals and to moving right away to ensure that 98% of families do not face a tax increase. we need to look at history. what we saw in the 1990s and 2000s, there was no relationship between lower marginal tax rates for the wealthiest among us an economic growth.

8:30 pm

first during the clinton administration, the top marginal tax rate was raised on the wealthiest individuals and the economy grew at its fastest rate in a generation. it added more than 22 million jobs. during the following eight years, the top marginal rate dax tax rate was lower, but economy never regained its strength from the reviews decade. job growth slowed and wages stagnated. middle-class families are vulnerable when the recession began at the end of 2007. i hope this hearing is helpful not just in this hearing, but across this country to people who are watching and waiting for congress to act. i will say more at the end about some of our members who are leaving. it has been an honor for me to

8:31 pm

serve as chairman of this committee and also served with my friend, kevin brady, as vice chair. he has been great to work with. i hope there'll be bipartisan success in congress. i look forward to working with him as i change seats in the senate for the next congress. -- in a sense for the next congress. i am grateful to our witnesses, whom i will introduce. before i do that, opening statements. >> i think the chairman for the recognition. this is the concluding hearing from the 112th congress. i'm behalf of the vice chair, kevin brady, on behalf of republican members and myself, we wish to thank you or your services on the committee. this unique committee with equally divided. people are used to seeing such

8:32 pm

division producing gridlock in washington, but senator casey and senator brady worked together and had bipartisan cooperation. joint economic committee has riced as a widely respected forum on debating issues. i think you, senator casey, for your leadership. -- i thank you, senator casey, for your leadership. i also want to recognize the retiring senator from this committee, the senator from new mexico and the senator from virginia. our first secretary of the treasury, alexander hamilton, observe energy is a leading character in good government.

8:33 pm

the president must lead in a divided government and must not advocate his or her -- not abdicate hor or her responsibility. president obama has the responsibility to propose a real bipartisan plan to avert the fiscal cliff that can pass both the house and the senate. withdrawing from the recommendations of the simpson- from thewing recommendations of the simpson- bowles commission, the president could propose a plan that would not only avert the so-called fiscal cliff, but also help us avert the fiscal abyss. if president obama were to offer such a plan, republicans would act favorably. going over the cliff is unnecessary. as it has been observed in "the wall street journal," the president is boxing in the republicans. he is offering them a deal they cannot accept.

8:34 pm

first, the president has repeatedly called for a balanced solution involving both revenue and less spending. what is obvious to the most casual observer is that this plan is not a balanced. the fiscal cliff involves nearly four dollars of anticipated revenue from higher taxes for every dollar of spending cuts, yet the president wants more revenue and fewer spending cuts. if we fell off the cliff, his plan calls for another round of stimulus spending. you have got to be kidding me. lackshe president's plan is any reform in our entitlement system. the unrestrained growth in entitlement system is driving deficits and driving the debt even higher than the percentage of our gdp. it is estimated to be as high as $128 trillion.

8:35 pm

even if they confiscate all of the income that excesses $1 million, we cannot pay for the entitlement commitments that the federal government has made. we have made promises to ourselves that we simply cannot keep. without some sensible entitlement reform, our credit rating will be downgraded again. we will become a country that none of us recognize. secondly, fiscal plans failed to achieve their government budget deficit or debt reduction goals. dr. hassett has examined fiscal plans in other countries. on average, unsuccessful plans proposed an increase in revenue and spending cuts. moreover, the higher revenues in successful plans were generally drawn from non-tax sources and avid sales and

8:36 pm

adjusted fees for -- such as asset sales and adjusted fees for government services. thirdly, the government argues that the 2001 tax cuts are extended, raising tax rates on the top 2% will not harm the economy because it will not affect consumption expenditures. however, analysts have analyzed the combination of expectation -- of the expiration of the 2001 tax reduction for the top 2% and the extension of the medicare act and capital income. under the president's preferred tax policy, the top rate would go from 35% to 49.9% and for ordinary income from 15% to 25%. the long-term consequences of president obama's tax policies would have a profound and

8:37 pm

negative affect. capital stock would fall. fewer jobs and lower wages resulting in higher taxes would harm the middle class. data reveals three important facts of high income earners. the taxes on the wealthy raise as much faster than on everyone else during economic booms, but they also fall much faster during economic bust. people report more income when tax rates are low and not when they are high. there are better ways to increase federal revenues than hiking tax rates.

8:38 pm

congress could enact a program of tax reform that would lower rates and eliminate interest reductions. the president could open up more federal lands and offshore areas for energy exploration. his administration could take a more balanced approach to new regulations. economic growth can help solve our fiscal problems if the economy had grown at the percentage as it has done in the past. the treasury could have collected an additional 650 billion dollars in fiscal year 2012. the deficit that would have fallen. still bad, but remarkably better than where we find ourselves today. republicans stand ready to work

8:39 pm

with president obama for a balanced and bipartisan solution. so far, no evidence of that. let's create a long-term solution that does not burden individuals and gives businesses optimism to go forward and invest in the american economy. then the economy can grow for all citizens. i look forward to the testimony of our witnesses. >> thank you. i will introduce our two witnesses. dr. zandi is the chief economist at moody's analytics. he looks at macro racquets and -- macro economics and public policy. he is the influential source of policymakers and businesses and journalists. recently he published a report assessing the challenges of approaching the fiscal cliff and the most effective way to achieve long-term, fiscal

8:40 pm

stability. he received his phd from the university of pennsylvania. that will be a recurring theme in these introductions. [laughter] dr. zandi, thank you for being here. dr. hassett is the director and senior fellow at the american enterprise institute. he holds a phd from the university of pennsylvania. his research includes the u.s. economy, tax policy, and the stock market. he is previously a senior economist at the board of governors at the federal reserve system. he went to that graduate school of business at columbia university. he has worked for both the george w. bush and clinton administrations. both of you went to the same university. i'm sure you can agree on everything today. dr. zandi first.

8:41 pm

>> thank you for the opportunity. it is an honor to be here with kevin, a good friend of mine. let me say that these are my own personal views. they don't represent the views of the moody's corporation. lawmakers have to resolve three issues -- first, the fiscal cliff. second, raising the treasury debt ceiling, which as you know is becoming an issue rarely soon. -- an issue fairly soon. third, achieving long-term fiscal sustainability. that is deficit reduction and tax increases and spending cuts that allow the gdp ratio to stabilize by the end of the decade. these three things need to be done now. in terms of the fiscal cliff, if policy is unchanged and we

8:42 pm

go over the cliff and there is still no change after that, the gdp in 2013 will 3.5 percentage points. subtract that and that is a severe recession. cbo and others are probably us are underestimating how severe that will be because confidence is very weak. it is unclear how the reserve would response to this. we need to scale back from the cliff. at the very minimum, the cliff needs to be scaled back so it is only a hit to gdp at 1.5 percentage points at most. if you have more of a drive than that, it it becomes it.

8:43 pm

-- if you have more vague d rag than that, it becomes unsustainable. the economy will weaken. the budget deduction will deteriorate. we are seeing a fiscal drag in europe. i would argue that we should smooth into this drag even more. make policy changes so next year the gdp is half of this speed limit. that would be consistent with extending an emergency program and some form of tax holiday. in terms of the debt ceiling, that needs to be increased. it would be nice to extend it at the next presidential election. it would be nicer to get rid of it altogether. it is anachronistic law that is a problem. it creates a great deal of uncertainty. as you can see, it can do a lot of damage to the economy. there are a lot of reasons why it is being considered to eliminate

8:44 pm

jig there are a lot of reasonable proposals being considered to eliminate that ceiling. it should be carefully considered. at the very minimum, we should push this to the other side of the election. we do not want to address the debt ceiling on a regular basis. it is damaging confidence. on fiscal sustainability, we need deficit reduction in the next 10 years of about $3 trillion. to get there, a balanced approach would be $1.4 trillion in tax revenue. half of that would come through tax reform and the other half through higher tax rates. $1.2 trillion in cuts to programs -- medicare and medicaid, social security, and other budget items -- that would leave you with approximately $400 billion in interest savings. at all of that together and you

8:45 pm

get $3 trillion. the spending cuts were implemented as part of the budget control act. if you add all of it up, if you go down the path i articulated, the spending cuts would be -- the revenue increases would be 2-1. i think it is very consistent in the spirit of simpson-bowles. it would be a good goal to achieve. it is doable from both an economic and a political perspective. finally, you need to nail this down. uncertainty is killing us. it is hurting business investments. it has not affected laying off decisions yet, but it will. if we do not nail this down, investors will bail and the economy will struggle.

8:46 pm

but if you address this problem reasonably -- we have made a lot of progress since the great recession. if we nail this down, we will be off and running. thank you. >> dr. zandi, thank you. dr. hassett. >> thank you. it is always a pleasure to appear before this committee. under your leadership, this has always been a collegial lace to testify. it is an honor to be here. my testimony is broken up into two parts. in the first part i described the short-term consequences of going off the fiscal cliff. in that section, i concur with

8:47 pm

dr. zandi that if we were to go off the fiscal cliff with no policy changes, then the near- term negative economic consequences would be significant. it would throw us into a recession. in the second part of my testimony, i will discuss the trade-offs we face between putting off the tough problems for tomorrow because we are worried about near-term effects. i think the evidence of the long-term effects of government debt to gdp ratio is quite overwhelming. it began with an early analysis who analyze economic growth that high debt levels. it has been confirmed that high levels of government debt shows low economic growth. these literatures can get more sophisticated.

8:48 pm

there is a paper that identifies a tipping point in gross debt to gdp ratio. if it gets above 73% and we are above that now, that has a very significant and negative affect on economic growth. to put the result in perspective, there is a simple tabulation that provides intuition for the result. if you run a deficit of 6% in gdp for the next 10 years, that would add to the gdp ratio. that increase would be a not by the end of the decade that would reduce the forecast. these effects are very significant. that growth story might be alarming, but the picture looks worse if you think of financial calamity.

8:49 pm

much of europe this year has been in turmoil because of the greek crisis. that in reality, the sickest european nations are in better shape than us. look at the struggles and other countries and take consolation in our relative stability. a recent study examined long- term projections for other countries debt burden. it found that the u.s. has a bigger adjustment than any of the european unions. it gives an urgency for us to act. it is also possible to theorize about how a continuation of these policies could hurt growth farther into the future. a recent paper shows that if we do not act on this, and we are basically producing a fundamentally different america.

8:50 pm

it suggests that we are going to move into a world by 2040 were economic growth in the u.s. is not what we normally expect to see each year. there is crowding out of unity by the government. that is how urgent it is. what should we do? there is another large literature that looks at fiscal consolidations. using my own study as an example and along with my two colleagues, our metric of success is that they achieve deficit reduction. we found fiscal consolidations that were very heavily weighted for spending were much more likely to be except the both

8:51 pm

then consolidations that were -- likely to be more successful than consolidations that were heavily weighted toward tax increases. we speculate that this is because we find this result because the tax heavy fiscal consolidations do not make tough choices on entitlements and because spending is more real when you lift the tax rates. it is easy to discuss reforms that could but u.s. and a positive trajectory. dr. zandi and i agree on the rough outline of what that would look like. the political challenge is a heavy one. if you look forward to the america we are creating, that we all have to agree that the stakes could not be higher. thank you, mr. chairman. >> thank you, dr. hassett. i would like to start with a comment about something we are probably not talking enough about. even as we are wrestling with trying to debt a handle on the

8:52 pm

fiscal cliff, we cannot lose sight of their urgent priority of making sure we have job growth -- job creation, to say the least. many of the components you have outlined -- that both of you have -- it comprised of the broad description of the fiscal cliff whether it is the expiring tax cut provisions, the expiring tax cut extensions, and spending cuts as well. if you consider more, which of those would you consider having the biggest bang for the buck in terms of economic impact of those that we are discussing here today? >> it is a given that we will

8:53 pm

extend the current tax rates for taxpayers that make less than $250,000 on an annual basis. that is absolutely necessary. when you consider the other things that are happening -- in terms of the bang for the buck, the emergency unemployment insurance program is very effective. it is small in the grand scheme of things. cbo is estimating it would costs per calendar year about $33 million. but the economic opportunity for job growth compared to the unemployment rate would be measurably more than that. we are down to go to million

8:54 pm

people in the program. it is falling each year. i expected to fall even more than that in the next year. there are also limits to how much emergency you can collect. there has been some good work that has come out of the reserve. it is a very significant positive. i think the payroll tax holiday has been very affective. it has very high bang for your buck. it gets spent. of hitting.skind it gets spent -- it is kind of

8:55 pm

hidden. it gets spent. it is designed in a way that helps lower income households. you might want to consider scaling that back. you can go to go 1%. remember making work pay? that was a good middle ground. it costs about half of the current payroll tax holiday. it is probably more affect it in the sense that it is designed to help more middle and low income households. that is a very effective program. >> dr. hassett, any comments on this question? >> thank you for asking that question. i disagree with my distinguished friend on this topic. keynes himself talked about the kind of place where we are right now. if you get onto a cycle of dependence on measures, it could lead to a downward spiral as the national get -- that gets bigger because you try to stimulate things with shots --

8:56 pm

one-time shots. i speculate that you might incur that the best possible thing we -- i speculate that he might conquer the the best possible thing we -- i speculate that he might concur that the best possible thing we can do right now for unemployed americans is fix our big problems. it would help if american businesses had clarity on what the future would look like. the sight of relief rally from such a thing would be worth better than anything you could get. >> i appreciated. i'm out of time, but i will come back to these issues in a moment. >> dr. hassett, an interesting opposition since you cannot ask questions. let me pose a question to you -- if the best thing that can be done is a long-term fix for

8:57 pm

our problems -- get out of this cycle that we are in -- would you agree with dr. hassett on that? >> i agree that we do not want to get into a cycle of dependency. we need to phase out the support -- the temporary support we have been running through the economy. in fact, that is what we have been doing. go back to 2009. by 2011, the fiscal policy was -- if you go back to 2009, adding two 0.5% pointed to gdp. by 2011, federal fiscal policy was neutral in respect to the economy. this year it will subtract from growth 8/10 of 1%. we have gone from fiscal stimulus to fiscal drag.

8:58 pm

all i am arguing for fiscal year 2013, we need to smooth into the fiscal drag. the government will be -- debating how much of a headwind it will be. we need to smooth into that drag. in the long run, we will be better off for it. >> is that a committee rule? >> it's not a rule. we will just keep it to a minimum. >> let me ask you for your response to his comment on the cycle of dependency. >> i think it is quite possible that is where we are. >> can i interject here? it feels that way to me. it feels like we are in a cycle of dependency. we are dealing with the 2011 debt limit and the stimulus from 2009. it is the same thing with

8:59 pm

different labels. i am having difficulty seeing a way out of this cycle, but i interested in your observations. >> the way that i think about this -- at moody's they have been careful to put in this perspective into their analysis. think about the way of what happens when you change the way you are playing the game. if you decide to spend a lot this year or mail checks to folks this year, that has a multiplier effect. you might get 2% gdp growth this year. but if you take that away, you are starting out with gdp growth 2% lower. there is a third phase where you need to pay for it.

9:00 pm

it is in the negative. in the end, you will have to pay something. you see that in the long run cbo analysis of these policies. we are in the hangover phase. i can say that there is a way out and it is very promising. we need to recognize that we are out of the emergency period. if we can fix the problems, we can get out of the hangover. >> the president is proposing the 47% spending cuts and 57% spending increase. why in the world would be even

9:01 pm

consider the president posted plan under the scenario that you described? >> the argument against our paper being a guide is that there are many small countries that may be have to be more aggressive about spending because people who lend them the money might head for the exit quicker. if you want to base our consolidation on the things that have succeeded in the past, we would be at a certain percentage of spending. there is great comfort that it would be successful. there is argument that we might be able to handle having bigger revenue share of that. if we copy the successful ones, we should surely almost succeed. if we have a half-and-half approach -- look at our paper when it came out almost two years ago.

9:02 pm

we said that the uk consolidation would fail. it had too much revenue. as we are seeing now, millionaires and billionaires are heading for the exit. that is what we are going to see. >> thank you. mr. chairman, i yield back. >> i would like to congratulate the chairman on his election and the fine work he has done as chairman of this committee and to congratulate mr. brady on being selected as his chair of this committee and the next congress. for our distinguished witnesses, they agreed that what we need to do is have a long- term solution. i would like to ask dr. zandi how we achieve that. we are several million dollars apart from the president's proposal. how would you close that gap? outline the president's proposal and speaker boehner's

9:03 pm

proposal. how can we get people employed and move our economy forward? >> i apologize. there will be a fair amount of numbers here. the president's tax revenue proposal amounts to about $1.6 trillion over a 10-year period. that is from higher tax rates. roughly 600 billion are from some kind of tax reform. they are all reasonably good proposals. speaker boehner's proposal on revenue -- is roughly $800 billion in tax reform.

9:04 pm

we are about $800 billion apart on taxes. my view is that we should roughly split the difference. i would suggest $1.4 trillion in tax revenue. $700 billion would come through tax reform. we can discuss what that might look like. $700 billion would come from higher tax rates. the president would scale back one trillion dollars. we can talk about that. on the spending side -- does 600,000 -- speaker boehner has come forward with some proposals.

9:05 pm

i'm not quite clear on how much the spending cuts he has proposed. the president's proposal is short. to get to where we need to go, that $3 trillion target and fiscal stability, we need $1.2 trillion in spending cuts. that should be part of the process. we should do some things to reform social security. after the end of the day, it needs to be almost double of what he is proposing. if you sit down and do the

9:06 pm

arithmetic of spending cuts and look at medicare and medicaid, unless you're proposing a big and structural change in the program, which i do not think is on the table at the moment, it is difficult to get that cut. it is really tough. if you do a run rate of about $600 billion in cuts, that is ok. bottom line -- fiscal sustainability at the end of this 10-year horizon. if we do that, we are off and running here. >> my time is about to expire. dr. hassett, i would like to hear your analysis on how far apart we are and how we can close that gap. >> thank you. we have a tremendous opportunity to make sure that we

9:07 pm

hand off a thriving economy to our kids. i mentioned that it we were to run $600 billion deficit for the next 10 years, by the end of that, the debt -- it would lower our gdp forecasts. if we were to cut with the fiscal consolidations that $600 billion deficit to $300 billion, we would be buying future generations gdp growth in the long run. it is ultimately a question of what kind of world we want to live in 10 years from now. if you want to look like the way europe has been growing, we will have a small consolidation, such as the small consolidation

9:08 pm

proposed by the president. if you want to have the kind of growth that i hope we can have with a bigger consolidation, that one is being proposed by speaker boehner. >> thank you. >> i would like to focus on something that is probably more of interest to the economists and ordinary people. let's talk about ratios. what i heard you lay out, dr. zandi, was more of an ideal situation. they get you at roughly at $3 trillion. the negotiations over last year's debt ceiling -- the new number would really be 1-1.

9:09 pm

that is not actually my question. i want to get to now. we have looked at the president's offer. we haven't found any spending reductions at all. we found the $1.6 trillion tax increases. we saw the extension of the unemployment insurance, which is an increase in spending. the delay in the spending cuts and no reform in entitlement whatsoever. do you think the president's

9:10 pm

current offer gives us the 2-1 test? >> no. he needs to come up with roughly $600 billion more in spending cuts over the next 10 years. i think that there are significant reforms in medicare, medicaid, agricultural subsidies, and other programs in the budget. those are difficult things to implement. it takes a lot of guts to propose those things. i would not discount them. they are important. to answer your question more specifically, we do name or spending cuts to get to my ideal. >> policymakers need to reform entitlements. i do see members of the other

9:11 pm

party -- most notably, mr. hoyer --he said, not now. they are on the table for a later discussion. i have been disappointed that a lot of the discussion seems to be on the revenue side and not really on the cutting side. really quickly, the debt ceiling. there is something about your testimony that caught my attention, which is your support for the initiative offered by senator rob portman. lawmakers can adopt a version of the so-called dollar rule to address the 2011 debt ceiling. policymakers could agree at the beginning to cover that here -- year's budget.

9:12 pm

they could -- adopting some form of this rule would be a good safeguard. i appreciate his comments. isn't this exactly what we did that now everyone is trying to get out of? we have a dollar of spending reductions. 1.2 is already in place. the other is in the sequester. isn't that what we did? if that isn't a good idea, why are you and the others now suggesting it is not a good idea? >> let me say a few things. first, the broad context. we need to get rid of the debt ceiling law. it is agonistic. we need to get rid of it.

9:13 pm

i suggest that some version of the dollar for dollar rule should be incremented. at least considered. it does not need to be one-for- one. it could be 50%. that is not going forward. my view is that we need to nail down how we can get to fiscal sustainability. get rid of the debt ceiling law. we need some form of budget rule to make sure that some discipline going toward. >> structure. >> yes, structure.

9:14 pm

we need to show people that we will stick to this plan. >> thank you. >> thank you very much for being here. i appreciate your testimony. dr. hassett, dr. zandi has indicated that he inks the debt limit crisis we had in august 2011 was bad for the economy and the country and that we should avoid it for the future. do you agree with that? >> first, yes. i think the best testament of this has been done by co- authors who have a very cool index of economic uncertainty. it is a very innovative paper. they estimated that the debt

9:15 pm

limit struggle probably subtracted about 1.5% from gdp growth during that summer when it was happening egos of the uncertainty and inactivity that was caused by levels of uncertainty. each time we go through that, there are consequences. i would like to add if that is what it takes to get spending under control, we need to concede that in the long run there will be a benefit, which means we do not have these deficits. in the fullness of time, whether a struggle last summer was worth it, if we have the spending cuts and deficits are lower, it might have higher economic growth in the long run because we went to that struggle last year. >> your position is that we should be ready to go through that struggle again and to call upon the national debt is necessary in order to enforce

9:16 pm

spending limits? >> that, of course, is not my position. we should never default on the national debt. the politics of debt reduction, which you on the better than me, are very difficult. i am not a political expert. if there is something we need to do that helps deficit reduction occur, i am not willing to stop process. >> you are saying defaulting of the national debt might be something we need to do now and then? >> no, sir. we do not default last summer. >> we did not. but we might in january of february. is it your position that we should be willing to default on the debt if that is necessary in order to force spending cuts? >> i would not be willing to default on the debt under any circumstances. look at the history of what has

9:17 pm

been done. there is a long history of using that debt limit as a moment to distract from the party in power. if we had an academic seminar on the impact of the that struggle and the fiscal policy, he would say that it was a negative thing. >> well, i have never until last year of august 2011, i have not seen any serious effort or serious threat made by the leadership of congress to refuse to give the secretary of treasury the ability to offer to meet obligations congress had adopted. i thought that was a new

9:18 pm

experience for us. it certainly was for me to see that happen. dr. zandi, you said you think that we need to repeal this law that tries to set a debt limit and concentrate more on taxing and spending policies that causes to raise the debt, as i understand? >> absolutely. it is a bad way to conduct policy. it is a problem. look at july and august of 2011. it was a mess. gdp downgraded the debt. it really had an impact. cbo is estimating the interest costs is costing us money. it is pretty clear that this is not going to get any better going forward. it will be worse. this is a really bad way of doing things.

9:19 pm

we need to get rid of this. having said that, we need budget rules. we need to find a way to be credible. the debt ceiling approach is the wrong way of doing it. >> thank you, mr. chairman. >> thank you, senator. >> i want to pursue that question a little bit. this is on my mind also. my experience is the political system find it awfully difficult to say no to constituents. with reelection in mind or a natural human tendency to want to please people rather than disappoint them. i had the privilege of meeting with christine lagarde from the imf. i asked about the reforms that

9:20 pm

were taking place in europe. i asked, would any of these reforms be taking place without europe being in a fiscal crisis mode? her answer was, absolutely not. unless the revolver is at the temple of the politicians with the finger on the trigger, they're not capable of summoning the collective will to tell the people that represent that they need to take steps to resolve a problem and will cause disappointment and pain to do so. my experience in the years i have had in politics was exactly that. we never would have gotten what we did in 2011 without the threat of defaulting on our

9:21 pm

debt. to think that we could put a structure in place today that perhaps we would all be comfortable with in terms of solving our long-term problems and be assured that 10 years or not that congress would not have modified that dozens of times to the response of into joints who are banging on the door and saying this is to develop much pain, we could hardly sustain a policy for months around here, let alone 10 years. if you want to fix the long- term situation, i think there is consensus that we cannot get from here to here to provide that kind of growth and what we want to hand off to future generations. we have to factor in a big

9:22 pm

factor of the political system here in the way politicians think and react. we need leverages in order to address that. i'm not really asking for a response. you have already answered to that. you have stated your position. i just wanted to add my two cents worth in terms of why i think it is important we have the leverage points. maybe there are other ways of doing this, but my experience is that the next congress or the current congress can undo that in a big hurry as the constituents line up outside their doors. thank you, mr. chairman. >> can i -- in response? >> yes. >> in the case of putting the revolver against the -- in the case of europe, we do not want to do this on a regular basis. that'll be a problem for our

9:23 pm

economy. people will not be engaged unless they have clarity in this thing. i have more faith in this institution. after the end of the day, you do the right thing. if you look at the history of this body, it roughly comes up with the right answer. we have not dealt with the debt ceiling since the beginning of this country. i think we are very capable and we can do it. >> i will respond by saying that we have been trying to deal with our cascading debt and deficit for decades. i would say that we have been far short of doing the right thing to look for a healthy fiscal future. >> thank you, senator.

9:24 pm

>> i agree that we usually do the right thing but only after we try everything else. the time has come. i see this as a scary time. we need to protect our fragile economy, but it is also an opportunity to move forward. my first question is based on your predictions -- what do you think the timeframe is for possible further downgrades from the credit rating agencies? >> this is my interpretation. i do not know for sure, but this is a guess from my

9:25 pm

experience. i think people outside of the beltway have a lot more faith in you than you do. there will not be a negative reaction. by the way, i would counsel -- you will get a better deal. >> in other words, a deal that does not mean much would not help us? >> in order to avoid a downgrade in the u.s. treasury debt, we need something lows to fiscal sustainability. we need to get to $3 trillion. if we fall short of that, that

9:26 pm

is a problem. >> ok. you brought up social security. don't we need more reforms to make that more solvent? if we were to embark on that and set up a commission, i think there is a lot of talk of ok, we should do that. >> i think that is a perfectly reasonable way to do it. >> my colleagues said that in the near term he would rather see rates go up on the wealthiest americans because he believes it gives us a greater long-term chance to reform the tax code. do you agree with this assessment? also, do you think this is a wise course? i support going back to the

9:27 pm

clinton levels. do you agree? >> i think we need to do both. if you are going down my path, we need both. there is no way to get to that number with tax reform alone. if you consider we will not take away a charitable deduction and if your goal is not to raise taxes from lower and middle-income houses. there is no way to do the arithmetic. there is no good way of doing it to raise that kind of revenue. we need to do both. we need tax reform and we need higher tax rates on upper- income households. >> it seems to me you could do the tax rates at the end of the year because then you could make the kind of deal that you

9:28 pm

want. to some of the closing of the loopholes. you could bring the corporate tax rate down and work on the debt by closing the loopholes and subsidies. >> tax reform is complicated. nail down a framework and then go to work and try to figure this out. in terms of corporate tax reform, that is absolutely necessary. the goal would be to make that revenue neutral. you want to bring down those corporate rates. >> what did you think of senator coburn's assessment? >> i have a great deal of respect for the senator, but this, i disagree. it would accomplished very

9:29 pm

little in terms of economic efficiency. with unemployment still high and -- we need to seek ways to make ourselves a friendly place. i am very concerned that i have seen the president continues to say that 97% of small businesses would not be affected. it is a very misleading statistic. anyone who has any profit from a sale on ebay would have -- we would be calling them a small business. more than half of the income is in that bracket. i strongly disagree. >> they're willing to make some sacrifices as long as we really are on the right path. they see that as their own

9:30 pm

long-term liability. thank you to both of you. >> thank you to my colleagues from pennsylvania. i would like ask dr. hassett -- the president's proposal had some specifics. i think it is clear there is a headline tax increase that he wants $1.60 trillion. what the administration would describe is $600 billion in spending reduction. it looks like 200 billion of what they put under the 600 billion is revenue. fees and various other forms of revenue.

9:31 pm

that is not spending restraint at all. there is a deferral of the sequestration. i am not clear how long that referral is meant to be. for one year, that is $100 billion. then there is additional stimulus spending and other things that add up to about $100 billion. that is $400 billion in the way. you should legitimately deduct from the headlines 600 billion if he wanted to write what might be legitimate spending restraint. if you go back, $1.60 trillion of new revenue, maybe we have $200 billion in spending restraint, it is it fair to say that this is a 8 to 1 ratio? >> that is about right. >> eight times the spending

9:32 pm

restraint. >> that is right. there is some recidivism here in the sense that spending reductions have systematically been overstated in recent years by the president. it appears to me that there is a lot of tax increase and almost no spending reductions. >> spending programs that you launch, that money gets spent. promises of future savings? much less so. when the president talks about new stimulus spending, i am not sure the savings would materialize at all. in reality, the president's proposal is almost entirely of new taxes and virtually nothing that is specific of the spending restraint. your research suggests that the most successful point of

9:33 pm

consolidation are those in which the ratio is almost the reciprocal of that. >> i can say with absolute certainty that a consolidation that has the shape of the president's proposal would fail. in the economy that we have now, in that kind of a world, it is impossible to envision generating the kind of healthy economic growth that the government is willing to have the spending cuts we promise to do two years from now. we will be saying, we cannot afford to cut government spending because it will throw us into recession. >> that brings me to the next issue i would like to discuss. to get to the president's tax increase package that he is looking for, he is calling for higher marginal tax rates. in addition, a reduction in the

9:34 pm

value of deductions and other expenditures. higher taxes on capital gains, dividends. the way i count this up, if you include the limitations, the top marginal tax rates for some would be between 41 and 45%. that is just the federal level. we have states with varying income tax rates. some americans would be paying more than half of their income. it would exceed 50%. if the president got all the tax increases that he wants, is likely that could precipitate a recession? >> it is not only likely, it would certainly do so. it is cataclysmic. if we go from a 15% dividend tax, to 45%, that is ridiculously bad news for an

9:35 pm

equity markets. it is something we saw on the other side. call for response to the dividend tax reductions and there was a lot of positive movement. as a package, there is a question of how negotiations work and maybe you want to start negotiations with an extreme position, i cannot imagine anybody looking at proposal and not arguing that it would not throw us into recession. >> rather than taking an extreme that is very harmful, you look for areas where the other side to meet halfway. for instance, because of the political imperative that has been created, if revenue has to be part of this, shouldn't at least be generated in the way

9:36 pm

it does the least economic harm? in your view, would you do less economic damage by generating revenue through reducing the value of expenditures than raising marginal rates? >> if you phase it in far in advance, for example, changing social security benefits when i retire now, he would have a positive growth the fed right now from the spending cuts because she would give clarity to all the people worried about the future of america. >> my time has expired. >> good morning. health care inflation is a significant driver of medicare escalating before us, what do you think should be done to

9:37 pm

control that inflation? i heard what you said about medicare. that is -- no matter what you do, you still have this inflation going on. it is major. >> let me say a few things. health care inflation in the last couple of years has slowed quite sharply. it has been about 3.5%. it is very positive developments. some of that probably is due to the weak economy, which means less demand for services. some of its likely is do to the affordable care act. there is growing evidence of that. we do not know for sure. there are some positive

9:38 pm

experiences in the affordable care act that could reap benefits. the insurance exchanges, the independent payment advisory board. we will have to see how that works out. most encouraged about the cadillac tax. this is a tax on gold-plated health insurance policies for folks like me. i get a very good health care package. if i get sick, i am unfettered in terms of my health-care consumption. it will make it more costly and i will start shopping for health care. that will create more transparency and get the growth in health-care costs down. we do not know what is going to

9:39 pm

work, but there are some interesting new programs that have potential. we should see how those worked out before we engage in some very significant structural changes. like a voucher program. we may have to go down that path, but it is much too premature to do that. we should see how these developments work. >> following up, "if temporarily going over the cliff is necessary to achieving a good agreement, lawmakers should not hesitate to do so." how long do think we could stay over the cliff without doing significant damage to the economy? >> i think you could go into early february.

9:40 pm

by early february, it looks like you are not coming to a deal and investors began to discount the likelihood you're not coming to a deal, you will see stock prices decline, the bond market reacted. by mid-february, it would be doing a lot of damage. by the end of february, the debt ceiling, of really bad things will happen. you have about a month. a lot does depend on whether the treasury is permitted to freeze withholding schedules. i'm going under the assumption that they can and will do that. >> a bad deal -- no deal is better than a bad deal. going back to, i am curious about, given your findings, do you believe the tax cuts for the first $250,000 in income

9:41 pm

should be extended immediately? is there any reason that it should be tied to tax cuts for the wealthiest in our nation? >> i think there should be done as a package. i think it will create brinkmanship. the nailing down the tax code, nailing down the spending cuts, nailing down long-term sustainability, you have to do this all once. that is the only deal that works. >> you think that you can be done by the end of the year? >> no, i am skeptical. i think it can be done before significant damage. i am playing a political

9:42 pm

observer, but my guess is that we will have to go into next year. >> vice chairman brady. >> chairman, i apologize for being late. thank you for your leadership. you have been a terrific leader, a tremendous to work with. i appreciate your approach and how you handle yourself. thank you very much. i think there is a bit of consensus in the sense that it is irresponsible to voluntarily go off the cliff, but equally irresponsible to come to a solution that does not address the key issues facing us. spending discipline, of fixing a broken tax code, and dealing with our biggest challenges. economic growth works. average recovery in this

9:43 pm

recession might have cut the deficit to $430 billion. returning to the pre-2008 levels. what is missing today, we know consumer spending is above what it was before the recession. government spending is above what it was before the recession. business investment, that area is what continues to lag. in your view, do you think raising taxes on the two marginal rates as well as capital gains dividends, does that encourage more business investment in the economy? >> the threat of those increases is a very big negative. mr. brady, one of the things economists use when they teach graduate classes is something

9:44 pm

called the handbook of public economics. you had to study that, too, mark. i know i did. one of the later editions, there is a chapter on how taxes effect business spending. we go into a very gory detail about how negative this can be. if the dividend tax is going to go up, a lot of firms would be hurt significantly by that. they would be paring back their capital spending in anticipation of higher taxes in the future. businesses will look to the future when they decide what they're going to do. they are not investing. you see it's in the investment data.

9:45 pm

it is why this recovery has been so slow. businesses have a lot of cash and are not making a lot of investment. >> your point is this does not help the economy. >> you could go back to the writings, he was a scholar who identified very early on that business cycles, recessions, and recoveries tend to be driven by investment because consumers are pretty steady, but investments can be fluctuating. his view of the problem of stabilization policy was to try to stabilize investment and not to focus on consumption. one reason we have had such a disappointing recovery is that we have not address the fundamental reason why investment is so weak. we are a really unattractive

9:46 pm

place for investors to invest right now. >> why don't you just accept a higher tax rates? it would be politically very convenient. it does not solve the economy. it does not solve the deficit. it is not a serious deficit proposal. the credit rating agencies are looking for a plan that lowers the gdp to debt ratio. i do not think there is a magic number. social security, medicare, to find a sustainable path for word on them. do you think the president's plan adequately addresses the sustainability of medicare and social security? >> i think he needs to go

9:47 pm

further. i do not think it is enough. i believe the proposals are good ones. i think they are hard proposals to make because they're substantive. to achieve fiscal sustainability in the context of $3 trillion in 10-year deficit reduction, i think we need to do more. >> looking at the republican plan and the president's proposal, do you see any common ground? >> the common ground is that we're looking at the same proposals. cbo has scored a number of different approaches. i also think there is no general agreement in the context of the current discussion, we will not make any major structural changes to these programs. we will not block grant medicaid, and we will not voucher or premium support

9:48 pm

medicare. in this context, it becomes dollars and cents. this is not going to be easy. i would suggest that in this quest for more reform to medicare and medicaid, if we can say by the 10th year of the budget horizon that we are on the right path, i think that is ok. entitlement reform -- >> the number is whether we have solved the problem. >> entitlement reform is tough and you cannot do it in 10 years. this is a long-term problem. we should be thinking about this in a 20 or 30-year horizon. cbo scoring makes it incredibly difficult. we don't want it to force us to

9:49 pm

make -- >> i would like to take a step back and step in a slightly different direction from the fiscal cliff and talk more about long-term and medium-term economic realities we face. in your written testimony to this committee, you warned against kicking the can down the road indefinitely because of the adverse effect that might have on the economy. the medium and long-term impact it might have. i thought your analysis was definitely something we need to pay attention to. as you observed in the failure to make progress in this area now could signal that we have

9:50 pm

bigger troubles ahead. the moody's analytics model that you used breaks down about 2028. the reason it does that because at that point, the interest on our national debt will start to cripple our economy. we will be left without much recourse. i'm not sure there is a tax increase on the planet that could suddenly fix that. i'm not sure we could print money fast enough. if we did, we would go the way of argentina. i tend to think of this medium and long term risk as the fiscal avalanche. the cliff is something we are approaching now and we can see where it is. we know will hit the cliff. the avalanche is different.

9:51 pm

the only thing you know about avalanches, you know when the conditions are present. you know when the snowpack has built up to the point where it could happen. you do not know when it is going to happen, you just know it is coming. once it hits you, the avalanche becomes completely impossible to control. do you agree with this characterization about the avalanche? could you elaborate about that kind of threat? >> would you mind if i steal that from you? i will give you credit. i think it is right. i do think -- that is why what you're doing now is so important. this is a once in a generation opportunity for you to nail these things down.

9:52 pm

we're not that far apart. i really do not think we are. if you are able to put us on a credible path to fiscal sustainability, do it in a balanced way, i think we are golden. i think we will avoid that avalanche. if we do not do that, ultimately, it means we will never do it until we're forced by that avalanche. >> how soon will we need to do that in order to avoid the conditions? >> i do not know the answer to that. my model breaks down. it will happen long before that. >> it could happen within the next four or five or six years. >> here is the thing. the problem is, if we do not address this, we will be stuck

9:53 pm

in this slow growth netherworld of going forward. we will get nailed by something. i do not know what it is, but something bad is going to happen. that is going to be the thing that sets off an avalanche. >> a credit downgrade? >> something we are not even contemplating. we do not know what that will be, but it will happen. we will set ourselves up for that avalanche. that is why it is so important to get this right. >> what about a credit downgrade? if that were to happen, doesn't that call into question all kinds of things? money market funds and other types of investment funds are chartered to invest only in a certain grade of funds.

9:54 pm

if all the sudden u.s. treasuries were downgraded, wouldn't that have a pretty significant the fact on where we are relative to the avalanche? >> if there is downgraded treasury debt, this would likely trigger other downgrades. bank debt, they will get downgraded. jpmorgans of the world. money managers have in their relationship with their clients agreements not to invest in bonds that have rates below a certain grade. they will have to divest themselves because of the downgrades. this will cause problems in the credit markets. the credit markets will ultimately adjust. the reality has not changed.

9:55 pm

you will see hedge funds and private equity firms, but that is the process. it will take time. between now and then, it will create a greater amount of turmoil. it is what this means. it means that we do not have the political will to nail this thing down. and we will not. people will recognize that and we will go nowhere. >> if you want to preserve the entitlement, get us to balance. >> get us to sustainability. >> thank you, mr. chairman. >> i have one more question. i know we could be here a while if we had the time. i am grateful for the patience of witnesses. i was looking at the testimony and on page 8, he walks through the question of this balance of

9:56 pm

how you do the balance between cuts and revenue. in the second full paragraph, he says, using a range of different methodologies, the average unsuccessful fiscal consolidation relied upon a 53% tax increase, 47% spending cut spurred a successful consolidation consists of 85% spending cuts. i want to get your sense of that. whether you agree with that 85- 15. if not, why not? what would your approach be? >> i respect kevin's work a lot. i think that number varies considerably depending on the country and it depends on where the economy is in the business

9:57 pm

cycle. it also depends what the reserve is with respect to monetary policy. it is one thing if interest rates are 4 or 5%. it is another thing if we are at 0. there has been a lot of really good work revolving around these issues and trying to get good benchmarks for fiscal consolidation. a really great paper came out of the imf the last couple of days on this issue. it makes a very strong case that there was a fiscal speed limit. you cannot have too much fiscal consolidation too quickly. it becomes counterproductive. this balance between tax and spending in the context of the u.s., particularly when the economy is weak, the spending multipliers, when you cut spending, they are very large, much larger them was previously

9:58 pm

thought. i did not buy into kevin's 85- 15. in the context of where we are today, that is not right. having said that, i would do something like that proposed. two-one kind of ratio. if you do that, that is balanced and it did system reasonably good place. it gets us to fiscal stability and avoiding the avalanche. it is still more spending than tax, but it is more balanced. the last thing i would say, we're talking about taxes and spending, this is an important point. tax reform is spending cuts. there is no difference. if i give you a mortgage interest deduction or cut you a check. no difference. from an economic perspective,

9:59 pm

they are one in the same thing. that is a spending cut. >> i do not have anymore questions. >> looking at our global competitors who find themselves in financial crisis showed more than 20 times in nine different countries, those countries cut what they owed in their spending and grew the economy at the same time. they did that because their cuts were large, credible, politically difficult to reverse. there were real and they were believable. it created the confidence to grow an economy. it was proven over and over again. that is the model for this fiscal cliff discussion, making

10:00 pm

both the cuts and the reforms that are real and credible and politically difficult to reverse. that is the only signal we can send. it is the right signal to send to investors that we're serious about getting our financial house in order. chairman, thank you. this is your last committee meeting and you will be missed. >> going back to the analogy of the avalanche, when we had the subprime crisis, and there was no warning. likewise, we did have the same type of avalanche come tomorrow. there is no more confidence, nobody buys are debt.

10:01 pm

-- buys our debt. we would have increased interest rates and huge economic problem. we have two things in front of us. not only the fiscal slope, but also the debt ceiling. treasury estimates at the end -- we have until the end of february. in solving it, would be better to put the debt ceiling in the package with the fiscal slope for a comprehensive solution? or would it be better to do them separately? >> they should be done together. this will not work if we break this thing apart. we need to scale back the cliff. we need to raise or eliminate the debt ceiling. we need to achieve fiscal sustainability. this needs to be a package. it has to be done very soon. >> i agree.

10:02 pm

>> i want to thank both of you for your testimony. >> thank you very much. i appreciate your good work and your leadership. thank you for your testimony. i think we made in 90-minute meeting. that is pretty close. that is pretty good. i want to thank both of our witnesses again for their testimony. by the way, without objection, the full text of your opening statements will be in the record of this hearing. we're grateful because it is clear to most americans we do have a substantial challenge with regard to the cliff. we know if we do not take the right steps, it could jeopardize our economic recovery. we cannot afford to lose ground on the gains we have made. i am confident we can get this done.

10:03 pm